An NRI is an Indian citizen residing outside India for more than 182 days in a financial year. OCIs and PIOs are also eligible.

Up to three residential properties. No limit on commercial properties. Agricultural land, plantation property, and farmhouses can only be inherited or gifted.

No. NRIs cannot purchase these but can inherit or receive them as gifts.

Yes, NRIs can co-own property with resident Indians, provided all legal and tax requirements are met.

Yes, but a natural guardian must execute the purchase on behalf of the minor, and all legal formalities must be fulfilled.

Passport and visa/OCI card

PAN card

Overseas and Indian address proof

NRE/NRO account details

POA (if not present in India)

Sale agreement, title deed, and all property approvals

Not mandatory, but highly recommended if you cannot be present in India. It must be notarized and, if executed abroad, attested by the Indian consulate.

Check title deed and encumbrance certificate

Ensure RERA registration (TNRERA)

Confirm local authority approvals and up-to-date tax receipts

Yes, a PAN card is mandatory for all property transactions.

RERA registration ensures the project is legally compliant, protects buyers from fraud, and makes dispute resolution easier.

All payments must be through NRE, NRO, or FCNR accounts. Cash transactions are not allowed.

Yes, most banks offer NRI home loans. Repayment must be from NRE/NRO accounts in INR.

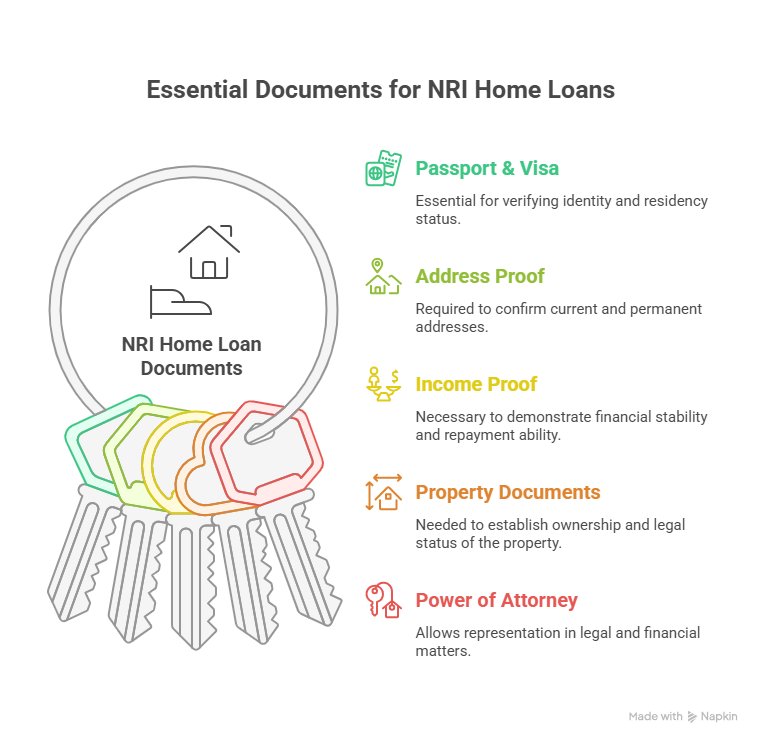

Passport, visa/OCI card

Address proof (overseas and Indian)

Income proof (salary slips, bank statements, tax returns)

Property documents

POA (if applying from abroad)

A quick visual checklist of the key documents every NRI needs when applying for a home loan in India.

Yes, as long as funds are remitted through legal banking channels into NRE/NRO/FCNR accounts.

Stamp duty and registration charges

TDS on property purchase (1% from resident seller; 20% from NRI seller)

Capital gains tax on sale (20% for long-term, 30% for short-term)

TDS on rental income (30%)

Up to USD 1 million per financial year after taxes and documentation.

Use NRE/NRO accounts and submit Form 15CA/15CB.

Yes, if your Indian income (including rent) exceeds the exemption limit or to claim TDS refund.

The Double Taxation Avoidance Agreement (DTAA) prevents NRIs from being taxed twice on the same income in India and their country of residence.

1. Define goals and budget

2. Shortlist and verify properties

3. Arrange funds and loan

4. Sign sale agreement

5. Register property and pay stamp duty

6. Take possession and update records

Step-by-Step Guide for NRIs to Buy Property in Chennai

Yes, through digital tools, POA, and property management services.

Market volatility

Legal disputes

Delays in possession

Currency exchange risks

Hire a property management company

Use a trusted POA

Choose projects with maintenance and rental management

Immediately consult a legal expert in India, gather all documentation, and consider filing a complaint with RERA or consumer courts.

Choose RERA-registered, gated communities with good amenities and security.

Yes, joint ownership is allowed and often recommended for succession planning.

Work with reputed developers like DRA Homes

Consult legal and financial advisors

Use digital tools for virtual tours and verification

How to overcome fear of buying a house

Register with local authorities

Set up utilities and maintenance

Update address in key records

Downloadable Checklist: NRI Property Buying Checklist for Chennai

Document Verification Guide: Step-by-Step Guide for NRIs

Tax Calculator: Income Tax India

Project Verification: TNRERA

Project Verification:

Contact DRA Homes for personalized support on any NRI property concern.

![]()

Link Copied!

Link Copied!